Fall is almost here. The air feels cooler, the leaves are beginning to change color, and Starbucks is serving Pumpkin Spice Frappuccino’s again! Also, school is back in session, so by most accounts, Fall is already here.

Fall is almost here. The air feels cooler, the leaves are beginning to change color, and Starbucks is serving Pumpkin Spice Frappuccino’s again! Also, school is back in session, so by most accounts, Fall is already here.

Recently, in my first period class, I was seated with a group of not-so-savvy shoppers. It seemed to me that their biggest problem was not having a budget. They complained about how quickly their money disappears when they go out. When I suggested to one of my classmates to consider a budget, her response was, “Budgets?! I don’t do budgets. I spend on the things I like, when I see them.” Another classmate said that when he gets his paycheck, he’s overwhelmed by the things he could spend his money on.

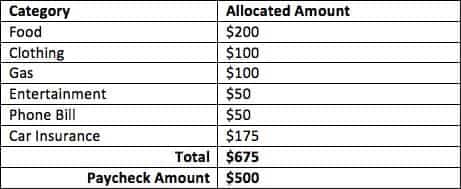

You don’t need a Master’s Degree in Finance in order to create a budget. Let’s start by considering your income. Let’s say you make $500 dollars in a month. Next, think about what you spend your money on. If you have no idea where your money disappears to, check your statements and categorize by the places you shop. For example, if Starbucks, Safeway, and Subway appear on your statement (thank you English teachers for teaching me alliteration!), then you should categorize them as food. You’ll want to find the average amount you spend monthly for each category. To find the averages, total up each category for a span of at least a few months, then divide those totals by the number of months you’re working with. Categories like food, clothing, gas, and entertainment are examples of variable expenses, meaning that they might change each month. You might spend more on clothing in August then you would in February. That’s why they’re called variable. For this example, let’s say that on average, you spend $189 on food, $86 on clothing, $65 on gas, and $40 on entertainment. Then there’s your fixed expenses, which include bills such as a phone or car insurance. Let’s say you spend $50 dollars on your phone bill and $175 dollars on your car insurance. You’ll want to make a table like the one below. You can do this on paper or you could download a spreadsheet app on your phone or laptop to create your table. Find your averages and add them to the table along with your fixed expenses.

Notice how I allocated an amount for each variable expense category that is slightly above their averages. This is to be sure you have enough for those extra expenses when they arise. The totals here have exceeded the paycheck amount. Based on this budget, you would spend your entire paycheck, and then some. What this means is that you have to intentionally cut back your spending within some of your variable expenses categories. You can change your spending habits but not your fixed expenses. This is why budgeting is important! You can easily see why you might be running out of money each month and start making changes to stay on track.

Now that you’ve established a budget, stick with it! If the allocated amount for a certain category is less then what you need, find another category that you can cut back on. Make it work for you. It’s your budget!

Luis Dominguez

Student Social Media Intern

1st Nor Cal Credit Union